carried interest tax changes

In-kind distributions and carried interest waivers. On July 27 2022 Senate Majority Leader Chuck Schumer D-NY and Senator Joe Manchin D-WVa released.

In 2011 Convey Sponsored A Tax And Regulatory Survey Carried Out By The Institute Of Financial Operations During A Time Of U Tax Infographic Accounts Payable

Under this proposed bill.

. Carried Interest Changes in the Inflation Reduction Act of 2022. Friday July 29 2022. Venture investors shrug at proposed changes to US carried interest taxation.

At most private equity firms and hedge funds the share of. Senate Majority Leader Chuck Schumer D-NY and Sen. Congress has indicated that it desires to change the law to further close the carried interest loophole ie.

November 1 2021. The significant tax changes to the treatment of carried interest introduced in this bill track the mark-up of the Build Back Better Act that came out of the House Committee on Ways and Means last September 2021. This article discusses carried interests how they are taxed and how if passed the proposed changes to the taxation of carried interest would affect real.

Joe Manchin D-WVa announced an agreement to add the Inflation Reduction Act of 2022 to the FY2022 budget reconciliation bill and vote in the Senate next week. Carried interest has historically been taxed at long-term capital gains tax rates which can be significantly less than ordinary income tax rates. The proposed amendments would be effective for tax years beginning after December 31 2022.

Carried interest is the percentage of an investments gains that a private equity partner or hedge fund manager takes as compensation. A compromise in Congress is forming among Democrats to tinker with the tax code generate revenue by other means and. The Tax Cuts and Jobs Act implemented rules that prohibit taxation at more.

Many presidential administrations in the past have attempted to make changes to the way carried interest is taxed. The Implications for Investment Advisors. The current tax treatment of carried interest is the result of the intersection of several parts of the Internal Revenue Code IRCrelating to partnerships capital gains qualified dividends and property transferred for services provided.

Carried interest is paid to a general partner of a private equity fund when the fund sells a business for a profit. While the Stop Wall Street Looting Act a comprehensive bill first introduced in 2019 never made it out of committee in a Republican-controlled Senate the current legislative movements in a now Democrat-controlled Senate and House have gained significant momentum. The proposed legislation would among other things significantly expand the scope of Section 1061 1.

If enacted into law the Inflation Reduction Act would significantly affect the ability of investment advisors to receive preferential tax rates with respect to their carried interests. Under current law a taxpayer whose carried interest is subject to section 1061 may still recognize long-term capital gain with respect to assets that have been held for at least 3 years. The bill directs the Treasury Department to issue regulations to prevent the avoidance of short-term capital gain treatment under Section 1061 and specifically mentions two techniques commonly used by fund managers.

Under current rules carried interest on investments held at least three years can qualify for long-term capital-gains tax rates which are well below those applied to. Arguments to change the tax treatment of carried interest are often based on the economic. The current three year holding period required to achieve long-term capital gain treatment for carried interest payable in.

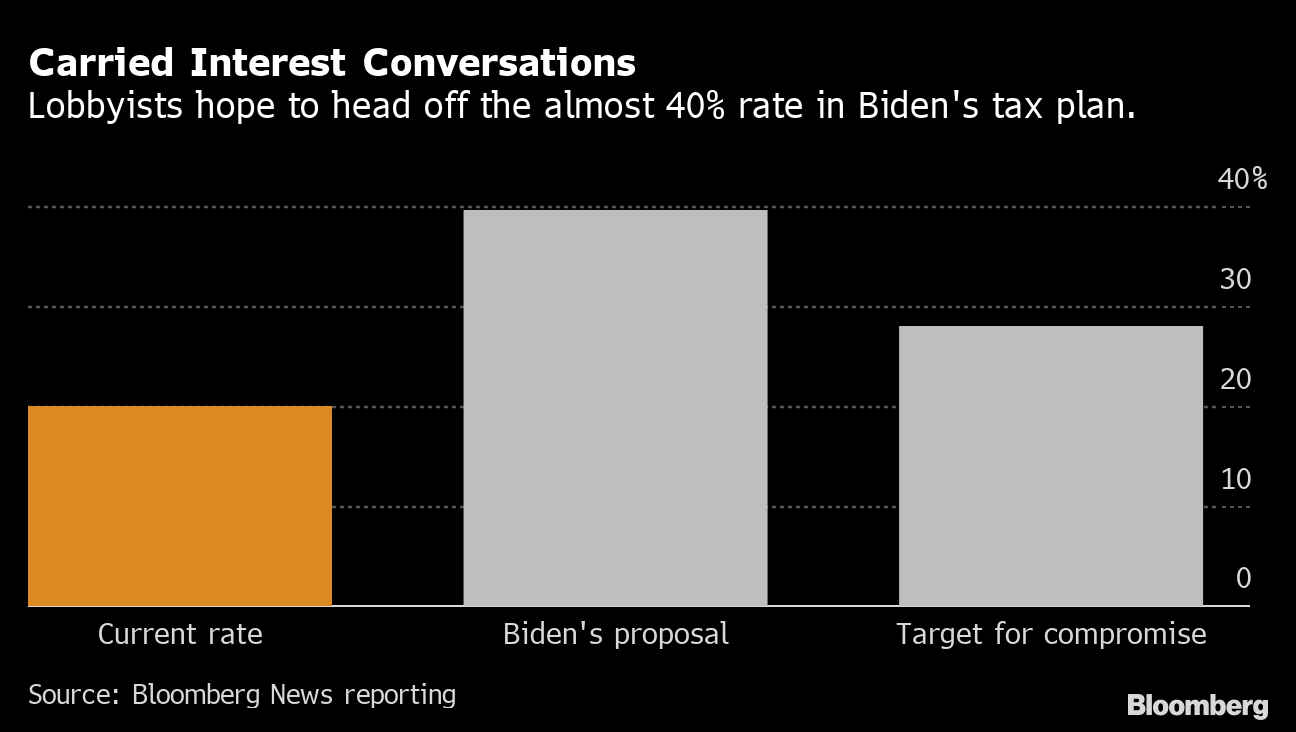

If it passes the changes to the carried interest provision along with the establishment of a corporate minimum tax rate of 15 would help fund the development of renewable energy projects. Code Section 1061 was enacted in 2017 to place limits on the ability of carried interest arrangements to be eligible for preferential long-term capital gain LTCG rates instead of higher ordinary. So far the lobbyists are winning.

The carried interest proposal would among. The carried interest proposals were previously set forth in the Build Back Better Act HR. Any ability for a service provider to receive LTCG rates from a partnership interest acquired in exchange for providing services and the deferral of some or all of the income until an exit event.

Carried interest rule changes could have a negative affect on the venture industrys inclusion. In his must-read new book Post Corona Scott Galloway calls. Carried interest has long been the target of lawmaker scrutiny.

The proposed rules would apply for tax years beginning after Dec. President Obama President Trump and President Biden have all wanted to eliminate tax treatment for carried interest. On July 27 2022 US.

The last time that carried interest tax treatment came under fire was in 2017. But private equity firms spend millions of dollars a year on lobbyists who fight any effort to change how carried interest is taxed. The changes would apply to tax years beginning after December.

Will Congress Close The Carried Interest Loophole Bdo

What Are The Consequences Of The New Us International Tax System Tax Policy Center

![]()

Fact Sheet Close The Carried Interest Loophole That Is A Tax Dodge For Super Rich Private Equity Executives Americans For Financial Reform

What Is E Way Bill Under Gst Goods And Services Internet Usage Goods And Service Tax

![]()

Definitive Guide To Carried Interest Book Private Equity International

Carried Interest In Venture Capital Angellist Venture

/dotdash_Final_Deferred_Tax_Asset_Definition_Aug_2020-01-dab264b336b94f939b132c55c018f125.jpg)

Deferred Tax Asset Definition

Pin Page

2

Carried Interest Tax Break Unites Pe Firms As Congress Takes Aim Bloomberg

What Are The Consequences Of The New Us International Tax System Tax Policy Center

Carried Interest Tax Break Unites Pe Firms As Congress Takes Aim Bloomberg

All About Minimum Alternate Tax Mat Alternate Minimum Tax Amt Deferred Tax Income Tax Health Education

Fact Sheet Close The Carried Interest Loophole That Is A Tax Dodge For Super Rich Private Equity Executives Americans For Financial Reform

2

Features Of Comparative Statics Microeconomics Study Assignments Helpful

Nog6e5fxqmna7m

Tax Optimiser Nps Perks Can Reduce Jaiswal S Tax Outgo By Rs 47 000 In 2022 Income Tax Saving Buy Health Insurance Income Tax

3pl Services Warehousing And Logistics 3pl Company In India Fit 3pl